Debunking the Claim: United Overseas Bank (UOB) Offers the Highest Return of 7.8% per Year

When it comes to investing our hard-earned money, we are always on the lookout for the best possible returns. Recently, there has been a claim circulating that United Overseas Bank (UOB) offers the highest return of 7.8% per year. However, it is important to examine this claim critically and understand the full picture before making any investment decisions.

Scottz Lip - The Snipe Investor

2/6/20245 min read

When it comes to investing our hard-earned money, we are always on the lookout for the best possible returns. Recently, there has been a claim circulating that United Overseas Bank (UOB) offers the highest return of 7.8% per year. However, it is important to examine this claim critically and understand the full picture before making any investment decisions.

Firstly, it is crucial to note that the financial market is dynamic and subject to various factors such as economic conditions, interest rates, and market fluctuations. Any specific return rate mentioned may not be a constant figure and can vary over time. Therefore, it is essential to consider the context and timeframe in which the claim is made.

While UOB may have offered a return rate of 7.8%, it is important to understand that this rate may not be available to all investors. Foreigners and U.S Persons can apply too. Banks and financial institutions often offer different rates based on the type of investment, the amount invested, and the duration of the investment. It is possible that the 7.8% return rate is applicable to a specific investment product or a limited-time promotional offer.

When evaluating investment options, it is crucial to consider the risk associated with the investment. Higher returns often come with higher risks. I read the website, conditions and checked with my relationship manager. The risk is pretty low with up to $75k insurance protection.

You need to meet the following criteria:

Be 18 years old at time of application

Put in $1000

Be ready to fork out $5 per month if your account has less than $1000 (this is the fall-below-fee)

Be ready to pay out an early account termination fee of $30 if you close the account with 6 months

Use UOB to pay your telco, utility, subscription, tax bills via GIRO (just need 3)

Get your HR to deposit your paycheck of at least $1600 every month

Spent at least $500 everyone on eligible UOB credit card (focus your spending on one card)

UOB Credit and Debit Cards that are eligible to earn bonus interest on the UOB One Account include UOB One Card, UOB Lady’s Card (all card types), UOB EVOL Card, UOB One Debit Visa Card, UOB One Debit Mastercard, UOB Lady’s Debit Card and UOB Mighty FX Debit Card.

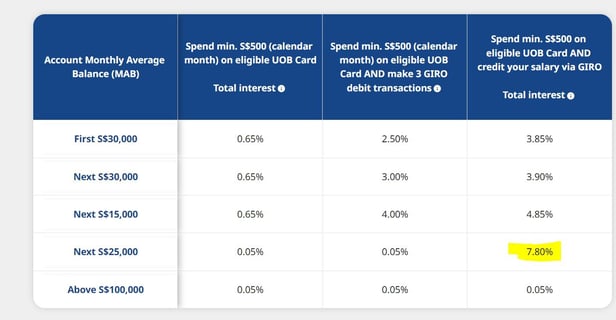

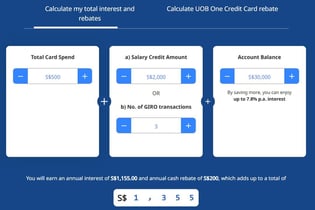

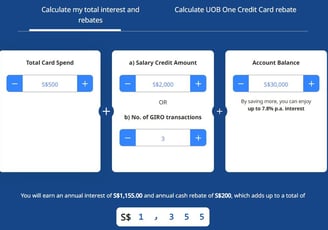

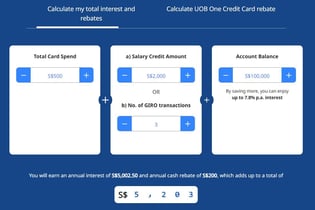

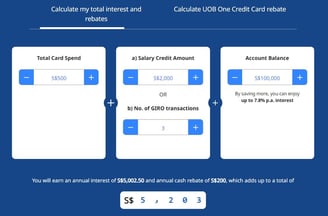

So, here's the big question....Do you actually get 7.8% if you deposit $100k? This means getting $7800 for the year (receiving $650 per month cashflow and passive income generating).

The answer is "NO". If you look at the details and the table below (from UOB website)

What exactly did you see? Let's do a breakdown of how 7.8% is arrived at. There are 5 tiers. The first tier is 3.85% for $30K, followed by 3.9% for another $30K, another 4.85% for another $15k (this is where you get safety with that $75k deposit insurance cover) and finally, the big 7.8% when you drop another $25k. Hey, this $25k is the risky bit and you are rewarded for your risk. The last tier is the most miserable at a meagre 0.5% when you drop your $101k. So don't really bother with anything beyond $100k.

It's dream to actually get 7.8% according to the marketing title with very little risk (at least to me) Therefore, it is necessary to assess whether the investment aligns with your risk tolerance and financial goals. It is advisable to consult with a financial advisor or do thorough research before making any investment decisions. Read about their offer (Disclaimer: I don't get any comms showing you their link). The online bank calculator shows you what you get for different amount of deposit. Starts as low at $1000, or go for $30k but do not drop in more than $100k. Is it better to invest with UOB right now? Yes. I will.

Short term Treasury bills and bonds are giving out about 2.7% to 3.8% as of this writing.

It is important to compare the return rates offered by different banks and financial institutions. While UOB may offer a competitive return rate, it is essential to explore other options in the market. By comparing rates, you can make a more informed decision and potentially find better investment opportunities.

So, the last thing on your mind is...What is the rate that you get if you drop $100k. You get 5% not 7.8%.

Download this excel sheet to do the calculations (I have put in the numbers). I am sure other banks will offer something similar as competition for your money heats up. You can use this to figure the actual return on your investment.

Lastly, it is important to read the fine print and understand the terms and conditions associated with any investment product. Some investments may have lock-in periods, penalties for early withdrawal, or other restrictions that can impact your ability to access your funds when needed.

In conclusion, while the claim that United Overseas Bank (UOB) offers the highest return of 7.8% per year may have some basis, it is essential to approach such claims with caution. Investment decisions should be based on a comprehensive evaluation of various factors, including risk tolerance, market conditions, and the specific terms and conditions of the investment product. Seek professional advice and conduct thorough research to make informed investment decisions that align with your financial goals.

Personal Opinion Disclaimer:

The opinions expressed here are solely my own and do not constitute financial advice. I am not a licensed financial advisor, and the information provided is based on my personal experiences, research, and perspectives.

It's important to recognize that individual financial situations vary, and what works for one person may not be suitable for another. Investment decisions should be made after careful consideration of one's own financial goals, risk tolerance, and circumstances.

I encourage readers to consult with a qualified financial professional for personalized advice tailored to their specific needs. My views and opinions may change over time, and I assume no responsibility for any actions taken based on the information provided.

Investing involves risks, and past performance is not indicative of future results. I disclaim any liability for any direct or indirect losses or damages that may result from the use of, or reliance on, the opinions expressed here.